Global Logistics in April: Rates, Energy, Routes, and New Supply Chain Risks

The defining feature of the month was not the disruption itself, but its nature. Instability has become constant, while the recovery of transport flows remains uneven and selective. The market is increasingly adapting to operating under constraints.

This has directly affected the economics of transportation and route configuration. Rising fuel costs are quickly reflected in freight rates and contract structures, while rerouting overloads alternative corridors and extends delivery times. At the same time, the role of geopolitics is increasing, as access to routes and supply stability increasingly depend on decisions made by governments and regulators.

Costs, lead times, and risks are changing simultaneously. This means supply chains now require not point-by-point optimization, but a broader review of management approaches.

Hormuz: A Local Conflict with Global Consequences

The crisis around the Strait of Hormuz has been ongoing for several months, but in April it entered a more acute phase. Threats of a full blockade, actual transit restrictions, and chaotic attempts to restore traffic have resulted in serious disruptions to shipping in the region.

Market response:

- Growth in the number of incidents and interventions in navigation.

- Vessel accumulation and forced route diversions.

- Service reductions and network revisions by carriers.

- Overloading of alternative routes and ports.

- Signs of flow fragmentation, with some traffic moving selectively or under restrictions.

Even after statements about the partial reopening of the strait, the market is not rushing back to a stable operating mode. Hormuz remains a key node for global oil and LNG supplies, which means any disruption affects fuel availability, price volatility, and supply chain stability, especially for Europe and Asia. In practice, businesses are now operating in an environment where the risk of delays, capacity imbalances, and rising operating costs has become a permanent parameter of logistics planning.

The Cost of Instability: How Fuel and Risks Are Reshaping Transport Economics

Escalation in the Middle East triggered a sharp increase in diesel prices, as well as aviation and bunker fuel costs, along with risks of fuel shortages, particularly in Europe.

This has created a systemic effect for the transport market:

- Higher ocean and air freight rates.

- The return of fuel surcharges.

- Contract revisions by carriers.

- Reduction of air services.

- Inclusion of war risk and fuel surcharges in ocean freight tariffs.

- Rising rates in ground logistics and capacity constraints.

Rate instability and the widening gap between contract and spot markets reduce cost predictability and strengthen carriers’ negotiating position. For businesses, energy instability makes logistics costs harder to forecast and complicates financial planning.

Restructuring Routes and Delivery Models

Alongside energy pressure, the market is massively restructuring routes. Shipping lines are reducing services in the region, introducing blank sailings, and redirecting cargo to alternative destinations. The use of longer maritime routes and multimodal solutions is increasing. This has already led to congestion in certain ports, particularly in India, higher pressure on inland infrastructure, and the emergence of new logistics corridors.

Multimodal transportation is becoming a necessity rather than an alternative, even though it is more expensive and more complex to coordinate. For global logistics today, route resilience matters more than speed or price.

Energy directly affects the configuration of supply chains, as changes in oil and LNG flows, as well as fuel availability, determine which corridors cargo will move through. Rerouting increases transit times and raises the likelihood of delays across the entire route.

Logistics Under Geopolitical Pressure

In April, government influence on logistics increased significantly — through sanctions, shipping controls, energy sector decisions, and fleet regulation. As a result, access to specific routes and even basic logistics services is increasingly determined not only by economics, but also by geopolitical decisions.

This is reflected in specific restrictions and decisions that directly affect the transport market:

- Threats of military blocking of the Strait of Hormuz by the United States and actual restrictions on Iranian oil transit.

- Expansion of sanctions pressure, forcing some countries to reconsider participation in port assets and logistics projects, including India’s decisions regarding Iranian ports.

- Stricter insurance requirements for vessels operating in the conflict zone and rising war risk premiums.

- Selective permits for passage through the strait for specific vessels and countries, creating unequal access to routes.

- Direct intervention by government agencies in supply chains, including decisions by U.S. defense authorities affecting federal supply chains.

- Failure of negotiations between the United States and Iran, which increased the risks of a prolonged energy crisis and further logistics restrictions.

As a result, the global logistics map is becoming more fragmented and less predictable. This changes the very logic of international transportation, where politics is becoming the same type of risk factor as cost or delivery time.

The Price of Instability: A Strategic Balance Between Risks and Opportunities

April’s developments showed that changes in logistics now go beyond transportation and directly affect business operating models. Companies need more flexible logistics models, route diversification, and a review of supply chains that accounts for new bottlenecks and instability in global flows. Under these conditions, the key priority is not only cost control, but the ability to ensure supply chain continuity.

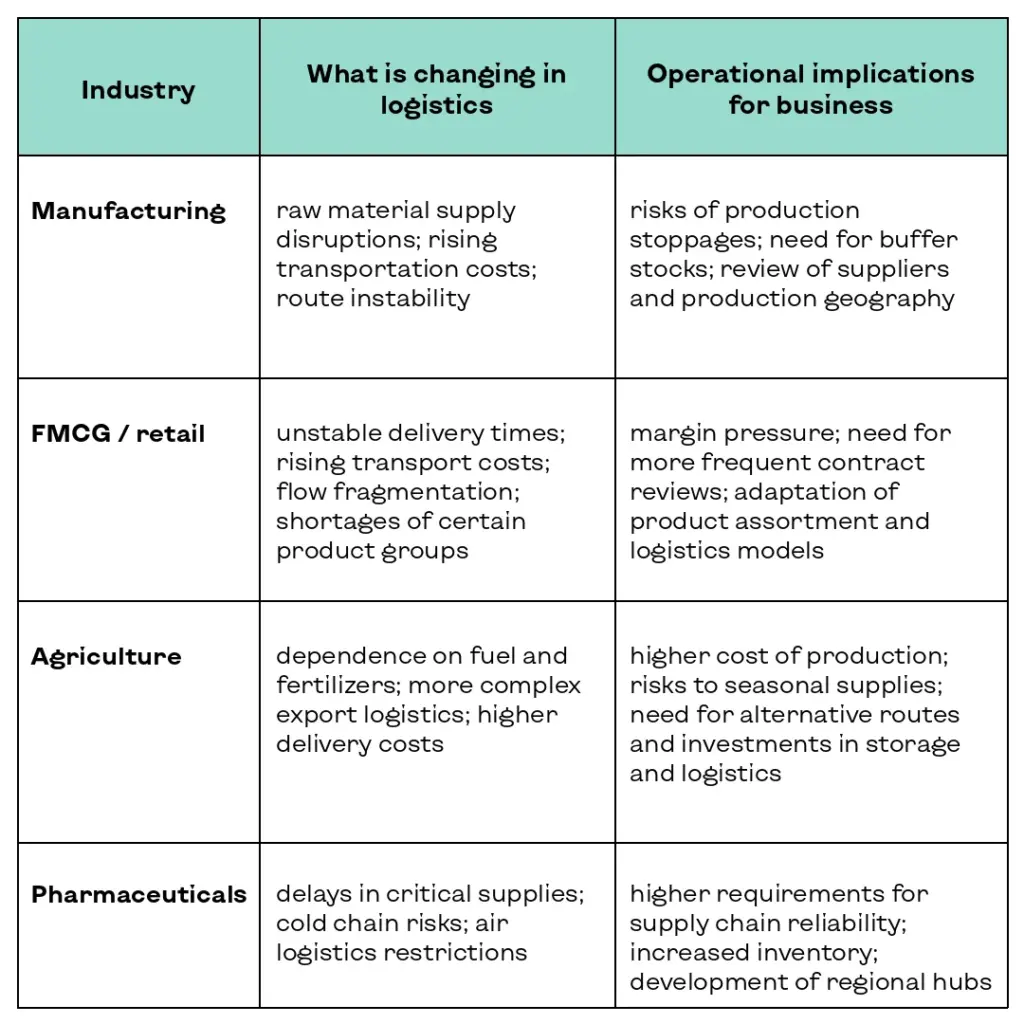

This is most visible in industries highly dependent on stable logistics, including manufacturing, FMCG/retail, agriculture, and pharmaceuticals.

Key Risks and Opportunities for Business

In the current environment, businesses are forced to balance critical threats with the search for new growth opportunities. The main risk remains the domino effect of the fuel crisis: a shortage of jet fuel in Europe and rising diesel prices are driving not only higher freight costs, but also carrier strikes that can paralyze domestic logistics in individual countries. In addition, the blocking of traditional routes creates bottlenecks at hub ports that are physically unable to process redirected cargo flows quickly enough, which increases delivery times. Sanctions, controls, and insurance requirements also complicate contract execution.

At the same time, the crisis opens potential opportunities for a technological and structural leap:

- Logistics cooperation. Stronger regional cooperation, for example between Middle Eastern countries and India, enables the development of new multimodal corridors that may remain effective even after the conflict ends.

- Digital visibility. The need to track cargo in real time accelerates the implementation of AI-powered platforms, giving businesses better control over inventory.

- The reassessment of production locations in favor of geographically closer regions reduces dependence on turbulent maritime routes.

SYNEX Logistics Perspective: Logistics in a State of Permanent Instability — How Businesses Can Operate in the New Reality

April’s events around the Strait of Hormuz confirmed a new reality for global supply chains: route instability, energy volatility, and geopolitics have become baseline variables, not temporary risks. This shifts the focus from a “lowest-cost” model to supply chain resilience, where the key factor is a company’s ability to operate under uncertainty and adapt quickly.

In practical terms, this means reviewing logistics models: more flexible contract terms, shorter tariff horizons, and alternative supply routes. The energy factor is already directly affecting all modes of transport, while rerouting creates additional pressure on infrastructure and forms new bottlenecks.

The response is logistics diversification: combining ocean, multimodal, and regional solutions, developing alternative corridors, and increasing transparency through digital monitoring.